Revolutionise Your Business with Blockchain Development & Implementation: A How-to Guide

December 13, 2023

Last updated: January 9, 2024

Table of Contents

Implement Blockchain In Business: Your Roadmap to Business Transformation

By 2027, the blockchain market is poised to reach an impressive valuation of 163 billion USD.

“Blockchain” has surged in popularity, especially within the developer and corporate world seeking operational efficiency. In today’s digital landscape, the realization of decentralization’s power has become a fundamental part of everyday operations. However, the technology that’s taken the world by storm may seem complex for businesses to grasp and implement.

But should entrepreneurs clear out from the incredible opportunities that blockchain offers? Absolutely not, as we’re here to guide you through this transformative journey.

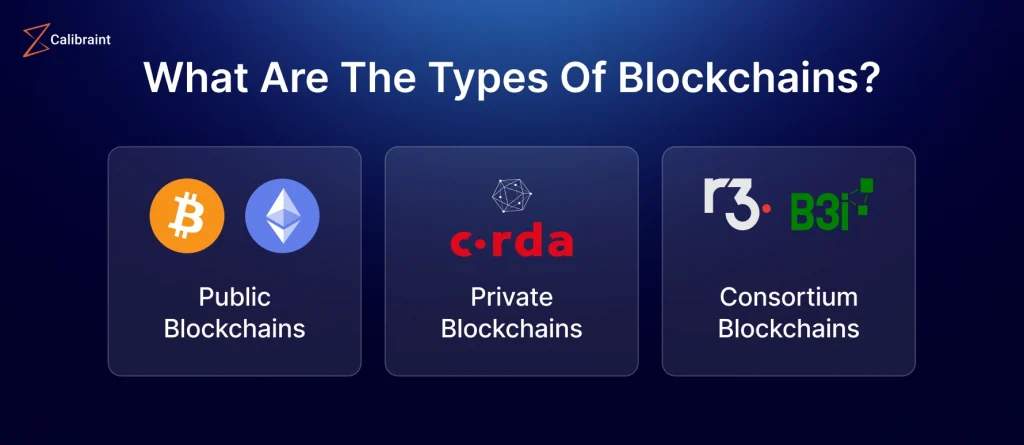

What Are The Types Of Blockchains?

There are primarily three types of blockchains:

Public Blockchains: Public blockchains are open and permissionless networks where anyone can participate, validate transactions, and create smart contracts. These blockchains are decentralized and typically rely on a consensus mechanism like Proof of Work (PoW) or Proof of Stake (PoS).

Examples of public blockchains include Bitcoin, Ethereum, and Litecoin.

Private Blockchains: Private blockchains are restricted networks where only authorized participants are allowed to validate and record transactions. They are often used by organizations for internal purposes, such as supply chain management or record-keeping. Private blockchains are centralized to some extent and provide greater control over the network. They may use different consensus mechanisms and are not accessible to the public.

Examples include Hyperledger Fabric and Corda.

Consortium Blockchains: Consortium blockchains are a hybrid of public and private blockchains. In a consortium blockchain, a limited number of participants (usually organizations or institutions) jointly validate transactions and manage the network. Consortium blockchains aim to strike a balance between decentralization and control, making them suitable for collaborative industry projects. Access to the blockchain may be restricted or permissioned, and consensus mechanisms vary based on the use case.

Examples include R3 Corda Consortium and B3i (insurance industry consortium).

These are the three primary categories of blockchains, but there are also variations and combinations, such as hybrid blockchains and sidechains, which aim to leverage the benefits of both public and private blockchains for specific use cases.

The Four Foundation Pillars of Blockchain Technology

The importance of blockchain technology for business relies on several key components and foundational concepts. Here are three main bases that support the growth and evolution of blockchain technology in business:

Cryptography: Cryptography is a fundamental building block of blockchain technology. It is used to secure data, create digital signatures, and enable authentication and authorization mechanisms. Public and private key pairs, cryptographic hashing, and digital signatures are essential cryptographic tools that underpin the security and integrity of blockchain networks.

Consensus Mechanisms: Consensus mechanisms are the protocols that ensure agreement among participants in a blockchain network regarding the state of the ledger. They play a crucial role in achieving decentralization and security. Popular consensus mechanisms include Proof of Work (PoW) and Proof of Stake (PoS), but various other mechanisms are being developed and tested to improve scalability, energy efficiency, and security. The ongoing research and development of consensus algorithms are vital to the advancement of blockchain technology.

Smart Contracts: Smart contracts are self-executing contracts with the terms of the agreement directly written into code. They enable automated and trustless execution of agreements, without the need for intermediaries. The development and improvement of smart contract platforms, such as Ethereum, Cardano, and others, are central to the growth of blockchain technology. Smart contracts have the potential to revolutionise a wide range of industries, from finance to supply chain management and beyond.

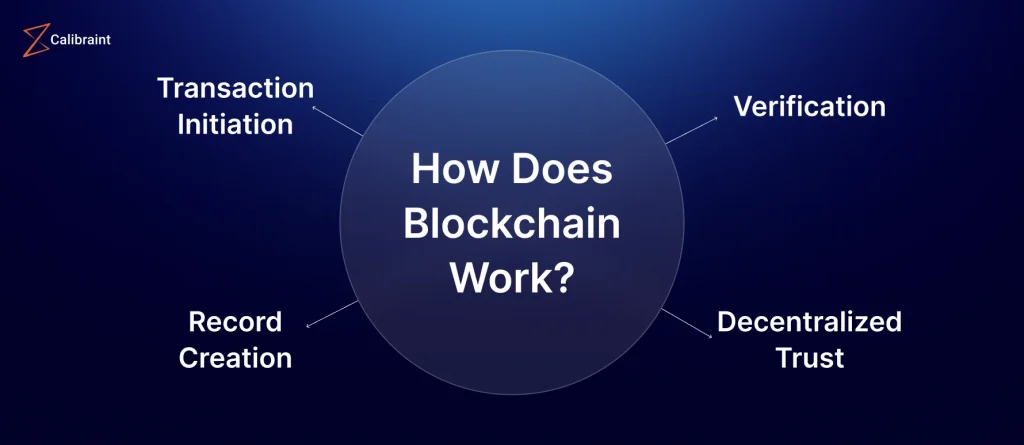

How Does Blockchain Work?

For businesses seeking to make the most of blockchain technology, it’s vital to grasp how exactly blockchain works:

Transaction Initiation: Users kickstart the process by creating requests to input data into the blockchain. This data can represent various actions, such as transferring assets, confirming identities, or documenting changes in ownership.

Verification: These transactions are then sent to multiple nodes (computers) on the blockchain network. These nodes work together to verify the transactions. In public blockchains, this verification is typically carried out using a consensus mechanism like Proof of Work (PoW).

Record Creation: Once a transaction is confirmed as valid, it gets added to a new block of data. This new block is then connected to the previous one, forming a continuous and unchangeable chain of data.

Decentralized Trust: To ensure trust and security, multiple nodes on the network must agree on the validity of each transaction. This decentralized verification process helps in preventing fraud and maintaining the integrity of the blockchain.

Is Blockchain the Turning Point for Startups and Enterprises?

Benefits Of Blockchain For Business

Blockchain certainly has the potential to be a turning point for both startups and enterprises. Its decentralized and secure nature can revolutionise various industries, such as finance, supply chain, healthcare, and more.

For startups, it offers a level playing field by providing transparency and reducing the need for intermediaries. Enterprises can benefit from increased efficiency, reduced costs, and improved security through blockchain implementation.

Empowering Startups

Startups often face challenges related to funding, credibility, and establishing a trustworthy reputation. Blockchain addresses these concerns by providing a secure and tamper-proof record of financial transactions. Through Initial Coin Offerings (ICOs) or Security Token Offerings (STOs), startups can raise funds directly from a global pool of investors, democratizing the investment landscape.

Moreover, blockchain enables startups to streamline various processes, from supply chain management to identity verification. Smart contracts, self-executing contracts with the terms directly written into code, automate and enforce agreements, reducing the need for intermediaries and minimizing the risk of fraud.

Enterprise Transformation

Enterprises, with their intricate networks and complex processes, stand to gain significantly from blockchain adoption. One of the key benefits is increased efficiency in supply chain management. By providing a transparent and real-time view of the entire supply chain, blockchain minimizes delays, reduces errors, and enhances traceability. This not only improves operational efficiency but also strengthens the relationships between different stakeholders.

Additionally, blockchain’s decentralized nature eliminates the need for intermediaries in financial transactions, reducing costs and processing times. Cross-border transactions become faster and more cost-effective, opening new avenues for global collaboration.

How Can Businesses Leverage Blockchain Technology For Tailored Solutions?

Blockchain technology offers businesses a versatile toolset for tailored solutions, providing a foundation for enhanced security, transparency, and efficiency.

Understanding Business Requirements:

Before diving into blockchain implementation, businesses must conduct a thorough analysis of their specific needs. This involves identifying pain points, inefficiencies, and areas where blockchain can bring value, such as transparency, security, and efficiency improvements.

Exploring Blockchain Applications:

With a clear understanding of their needs, businesses can explore diverse blockchain applications. Whether it’s supply chain management, smart contracts, or decentralized finance, evaluating different use cases helps tailor the technology to address specific pain points effectively.

Assessing Market Demand:

While formulating a blockchain strategy, it’s crucial to align with market demand. Identifying trends and understanding how other businesses or industries are adopting blockchain provides insights into potential opportunities and ensures the viability of the chosen solution.

Formulating a Unique Blockchain Business Idea:

To stand out in the competitive landscape, businesses should formulate a unique blockchain for business ideas that caters to their specific needs. This could involve creating a proprietary blockchain solution, partnering with existing platforms, or developing innovative applications that set them apart in the market.

Ensuring Regulatory Compliance:

In the landscape of blockchain regulations, businesses must stay informed and ensure compliance with legal frameworks. Understanding and adhering to regulatory requirements is essential for the successful integration of blockchain technology while mitigating potential risks.

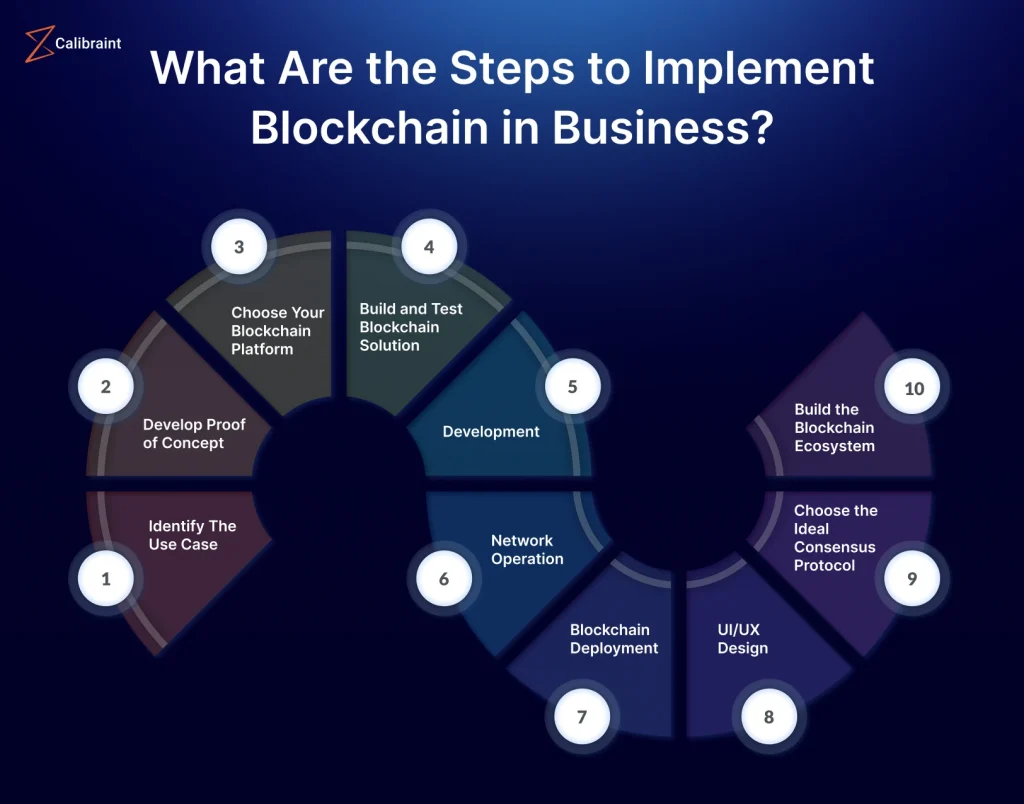

What Are the Steps to Implement Blockchain in Business?

Here is a step by step explanation on how you can implement blockchain in business.

Step 1: Identify The Use Case

The first step to implement blockchain in business is to begin by identifying potential use cases where implementing blockchain in business can improve the operations. Conduct thorough market research and start with a pilot project before scaling up. Careful planning and evaluation are crucial.

Step 2: Develop Proof of Concept (PoC)

Create a proof of concept (PoC) to test the feasibility and potential of the blockchain solution.

Ask questions about:

– How will it solve problems?

– How will it impact operations?

– How will it benefit the business?

Use the PoC to make informed decisions before full-scale implementation.

Step 3: Choose Your Blockchain Platform

The third step to implement blockchain in business is to select a suitable blockchain platform based on market research. Options like Ethereum, Hyperledger Fabric, Tezos, Corda, and Stellar offer different features. Consult with a Blockchain Development Company for expert advice on platform selection.

Step 4: Build and Test Blockchain Solution

Choose flexible blockchain technologies that align with business needs. Ensure breadth and depth of technology support, create smart contracts, and test your app on the network for seamless functionality.

Step 5: Development

The most time-consuming phase in the entire blockchain app development process involves multiple iterations of pre-release versions. This allows for the collection of valuable user feedback, enabling continuous improvements.

Once all bugs are addressed, and the app is equipped with the necessary features, obtaining approval from clients for the beta version becomes crucial. The emphasis should be on thorough testing, especially when dealing with the transfer of sensitive data.

Finding experienced blockchain engineers is another challenging aspect of the development process. If encountering difficulties in assembling a team with the required skills, consider exploring offshore software development companies. External developers possess the same level of expertise as in-house specialists and are readily available to contribute to your project on demand.

Step 6: Network Operation

Construct the first block with essential features, serving as the foundation of your blockchain network. Incorporate data validation, cryptographic hash, and timestamps.

Step 7: Blockchain Deployment

Deploy the blockchain network, ensuring functionality and enabling stakeholders to access and use it for secure operations. Set up a cloud server for hybrid solutions with on-chain and off-chain entities.

Step 8: UI/UX Design

If the MVP version is well-received, create a clear and attractive UI/UX design for your blockchain application. Developers will build the app based on the designed screens or pages.

Step 9: Choose the Ideal Consensus Protocol

Select a consensus protocol based on your requirements. Options include Proof of Work (PoW), Proof of Stake (PoS), Delegated Proof of Stake (DPoS), Practical Byzantine Fault Tolerance (PBFT), and Proof of Weight (PoW). Consider factors like security, energy efficiency, and speed.

Step 10: Build the Blockchain Ecosystem

As the number of stakeholders increases, build a thriving blockchain ecosystem by establishing terms of engagement, sharing costs and rewards, and implementing a sound governance mechanism. Embrace collaboration and transparency for a successful ecosystem.

Top 3 Pointers To Keep In Mind While Choosing Blockchain Development Services For Your Project

Blockchain development services play a pivotal role in empowering businesses to tap into the potential of blockchain technology for their growth and innovation. These services encompass a broad spectrum of solutions tailored to meet the specific needs of businesses.

Selecting a Trustworthy Development Partner

Choosing the right development partner for your blockchain project is a crucial decision that can significantly impact its success. When considering blockchain development services, businesses should prioritize reliability, expertise, and a track record of delivering high-quality solutions.

Key factors to consider when selecting a development partner include:

Experience: Evaluate the development partner’s experience in blockchain technology, focusing on similar projects or relevant blockchain use cases.

Portfolio: Examine their portfolio to assess the quality of their past work, specifically looking for successful implementations of blockchain applications.

Expertise: Assess the team’s proficiency in various blockchain platforms and technologies, ensuring familiarity with trends and best practices.

Client References: Request client references and testimonials to gain insights into the partner’s reputation and client satisfaction.

Scalability: Ensure that the development partner can accommodate your project’s scalability requirements as your blockchain application grows.

Evaluating The Companies Development Solutions

Blockchain Ideation: Evaluate the company’s role in assisting businesses in identifying use cases and crafting innovative blockchain business ideas.

Development on Multiple Platforms: Expertise in developing on various blockchain platforms, including Ethereum, Hyperledger, Corda, and more.

Comprehensive Blockchain Solutions: The company’s role in providing end-to-end solutions, from consulting and development to deployment and maintenance.

Blockchain Consulting: Check if the company offers strategic guidance and insights to align blockchain strategy with business goals.

Top Blockchain Developers: Research if the company has access to a talented team proficient in the latest blockchain technologies and trends.

Services Provided by Blockchain Development Firms

Blockchain development firms offer a comprehensive array of services to cater to diverse business needs, including:

Blockchain Consulting: Identifying viable blockchain use cases, defining business strategies, and assessing the feasibility of blockchain adoption.

Custom Blockchain Development: Creating tailored solutions for specific business requirements, such as decentralized applications (DApps), smart contracts, or private blockchains.

Integration Services: Seamlessly integrating blockchain technology with existing business systems and processes for smooth operations.

Security Audits: Conducting security audits and implementing robust measures to protect blockchain assets and data.

Tokenization: Developing and launching tokens for fundraising or asset management purposes, such as initial coin offerings (ICOs) or security token offerings (STOs).

Smart Contract Development: Designing and coding smart contracts to automate business processes, enforce agreements, and enhance transparency.

Take Your Leap Towards Blockchain Development With Calibraint

As businesses chart their course for the future, the potential of blockchain technology emerges as a catalyst for accelerated growth and innovation. Irrespective of a company’s size, blockchain extends benefits to all, transcending mere cost reduction. The route of blockchain in the business landscape holds promise, with both corporate giants and emerging startups increasingly integrating this transformative technology into their core operations.

If you’re contemplating on how to implement blockchain into your business framework, look no further. Calibraint stands ready to provide expert guidance and support, helping you transform your vision into reality. At Calibraint, we offer

Innovative Solutions: Calibraint’s expertise ensures that your business can leverage blockchain to craft innovative solutions tailored to your specific needs.

Competitive Edge: Stay ahead of the curve by incorporating the best solutions that set you apart in the market.

Global Integration: With Calibraint’s support, seamlessly integrate your business into the global blockchain ecosystem, opening doors to new opportunities and collaborations.

Enhanced Trust and Transparency: Experience a paradigm shift in how your business conducts and communicates, fostering stronger relationships with clients and partners.

Cost-Efficiency Beyond Basics: Calibraint ensures that your blockchain integration maximizes efficiency across various operational facets, contributing to overall financial optimization.

Seize The Opportunity – Ride The Wave!

As blockchain strides into various industries, its proven versatility signals a transformative era. To successfully implement blockchain in business, one should keep in mind the demands of strategic foresight, prudent financial planning, astute partnerships, seamless legacy system integration, and comprehensive employee education. The undeniable truth is that most businesses stand to gain from the enhanced security and automation bestowed by blockchain technologies.

While off-the-shelf solutions are on the horizon, organizations eager to lead the charge can create and install their bespoke blockchain solutions. To ensure a smooth journey into this digital frontier, companies are well-advised to enlist the expertise of the finest development teams.

Frequently Asked Questions

How Much Does It Cost To Develop A Blockchain For Business?

The cost to develop a business blockchain typically ranges from $50,000 to several million dollars, based on the complexity and features required.

Is Blockchain Suitable For Small Businesses?

Yes, blockchain is increasingly viable for small businesses, offering enhanced security and efficiency, although tailored solutions are often more practical than developing a full-scale blockchain.

What Are Some Blockchain Use Cases For Businesses?

Blockchain’s versatile use cases in businesses include:

- Supply chain transparency

- Smart contracts for legal processes

- Decentralized data storage

Categories

Related Articles

The Step-by-Step Guide for Roadmap to Web 3.0 Application in 2024

The internet has evolved significantly since its inception, from the static and centralized Web1 to the dynamic and interactive Web2. However, there are still some major drawbacks for users and creators which pushes the need for Web3. On the roadmap to Web 3.0 applications, a new paradigm of the internet aims to address these issues […]

13 Dec 2023

Cryptocurrency Prediction Platforms: Bridging the Gap between Investors and the Market

What are cryptocurrency prediction platforms? Cryptocurrency prediction platforms use AI, machine learning, or crowdsourcing to provide forecasts and insights on the future price movements and trends of various cryptocurrencies in the market. These platforms are useful for investors and the market, as they can help them make informed and profitable decisions in the volatile and […]

13 Dec 2023

Hello world!

Welcome to WordPress. This is your first post. Edit or delete it, then start writing!

14 Nov 2023